.png)

Most trading strategies look great, until you test them.

Indicators promise high win rates. Threads claim someone has found a reliable edge. Strategies spread quickly in trading communities and start sounding convincing.

But when those ideas are tested on real market data, many of them fall apart.

That gap between what sounds good and what actually works is where many traders lose money.

Trading ideas are easy to create. Anyone can look at a chart and come up with a rule that seems logical.

The problem is that the market often behaves very differently from what we expect.

Without testing, traders are mostly relying on assumptions, recent examples, or a few lucky trades. What looks like a solid strategy might simply be coincidence.

Testing ideas against historical market data helps traders see the bigger picture. It reveals how a strategy behaves across different market conditions, not just the few trades that happened to work.

This is where backtesting becomes useful.

Backtesting answers a simple question: Would this idea have worked in the past?

Instead of risking real money right away, traders apply their rules to historical price data. They check where trades would have entered, where they would have exited, and what the results would have been.

For traders, backtesting is just the beginning. After that comes a trading simulator or replay trading, where the same strategy is practiced in past market sessions before any real capital is used.

Platforms like FX Replay allow traders to replay historical markets candle by candle, turning past price action into a practical training environment.

Conseil de pro

Think of backtesting as the research phase of trading. It reveals whether an idea deserves attention before time and money are committed.

Backtesting is the process of applying a trading strategy to historical market data to evaluate how it would have performed in the past.

A trader begins with a rule set.

Par exemple :

Those rules are then applied to years of past market data.

Every trade that would have occurred is recorded. The results reveal whether the strategy made money, how volatile its performance was, and how large the losses became along the way.

Backtesting answers several important questions:

Markets are unpredictable, but patterns start to appear when rules are tested across a large number of trades.

Many strategies that look promising on a chart don’t hold up when you apply them to historical data. Backtesting brings those weaknesses to the surface early, before real money is involved.

This is how traders separate ideas that sound good from ideas that can actually survive real market conditions.

The process also reveals where a strategy tends to struggle. Some systems perform poorly when the market moves sideways. Others fall apart when volatility suddenly increases.

Understanding these weaknesses is important.

Strategies rarely fail without warning. In many cases, the warning signs are already visible in the backtest results long before any capital is put at risk.

Conseil de pro

Backtesting doesn’t guarantee success. It simply shows whether a strategy is robust enough to deserve further testing.

Backtesting follows a fairly simple process. The goal is to take a trading idea and see how it would have behaved in the past.

Start by writing down the rules clearly. This includes when to enter a trade, when to exit, and how much risk to take on each position.

Next, collect price data for the market you want to test. The data needs to be clean and accurate because mistakes here can distort the results.

Run the strategy through the historical data. This means checking every situation where the rules would have triggered a trade.

Track each trade that the strategy would have taken. Note the entry, exit, profit or loss, and any drawdowns along the way.

Finally, review the results to see how the strategy performed overall and where it struggled.

Backtesting can be done in two main ways.

Manual testing involves stepping through charts one by one and recording trades by hand. It takes time, but it helps traders understand how their strategy behaves in different market situations.

Automated testing uses code or specialized platforms to run the strategy across large datasets. This makes it possible to test years of data much faster.

Both methods serve the same purpose: finding out whether a strategy can stand up to real data before it is used with real money.

Replay-based platforms like FX Replay combine historical replay with trade execution, allowing traders to practice strategies inside real market conditions rather than only reviewing statistics.

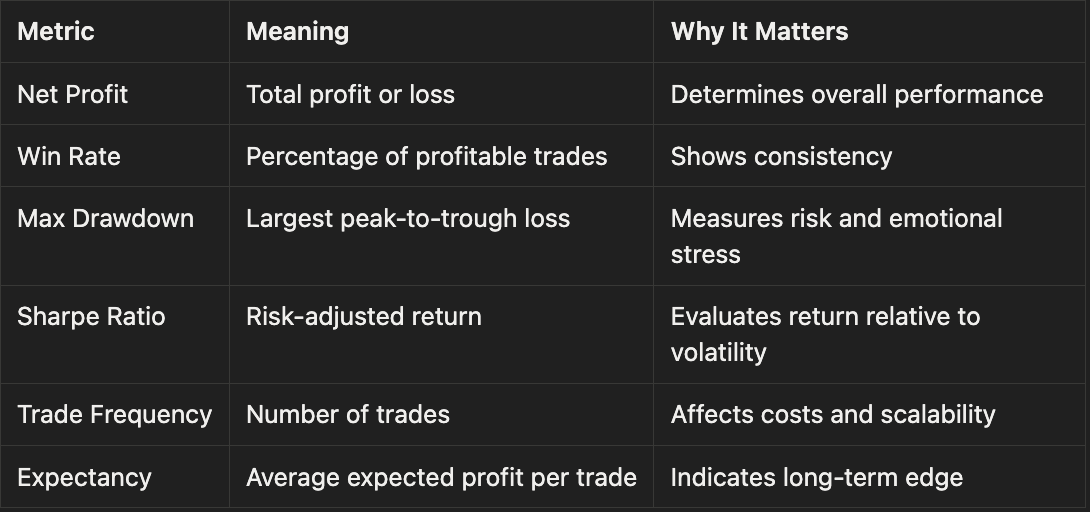

A backtest produces a lot of numbers. Some of them matter more than others when judging whether a strategy is worth pursuing.

Many traders focus too much on win rate.

A strategy can win most of the time and still lose money if the losses are large when they occur. Metrics like expectancy and maximum drawdown usually give a much clearer picture of how a strategy actually behaves.

Conseil de pro

A strategy that survives large drawdowns in testing is more likely to survive difficult market periods in real trading.

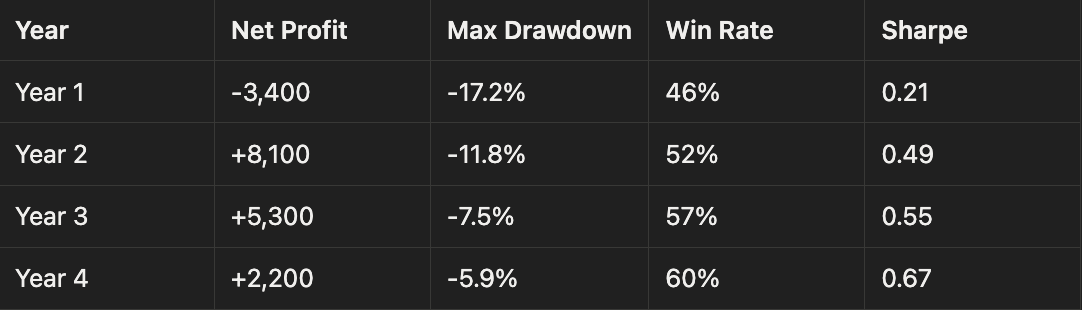

Consider a simple trend-following rule based on moving averages.

A trader buys when the 50-day moving average crosses above the 200-day moving average, often called a Golden Cross. The position is closed when the opposite crossover appears.

This idea has existed for decades. Some traders consider it a reliable trend signal, while others view it as outdated.

Backtesting helps clarify how it actually behaves.

Below is a simplified illustration using mock data to demonstrate how backtest results are often presented.

Even in this simplified example, a few patterns arise:

Backtesting does not eliminate risk, but it reveals the behavior traders should expect before committing real capital.

A well-run backtest can uncover several things about a strategy that are difficult to see from a few trades.

When a rule is tested across many years of data, certain behaviors may repeat. These patterns can suggest whether the strategy has a genuine edge or just benefited from a short-term market phase.

Backtests show how a strategy reacts during different environments, including crashes, volatility spikes, or strong trending periods.

Drawdowns often highlight the exact conditions where a system struggles, such as choppy markets or sudden reversals.

Large drawdowns also reveal how much capital a trader would realistically need to survive difficult periods without abandoning the strategy.

Backtesting evaluates the past. It does not predict the future.

Markets change over time. Economic conditions shift. A strategy that worked well in one period may struggle in another.

Hence, backtesting always has limits.

For that reason, backtesting should be treated as a stress test, not a forecast.

Conseil de pro

If a strategy cannot survive historical testing, it is very unlikely to survive real markets.

Backtesting can also mislead traders when the process is done carelessly. A few mistakes appear again and again.

Traders keep adjusting their rules until the results finally look good. Over time, the strategy becomes tailored to the dataset rather than reflecting real market behavior.

Real trading involves commissions, spreads, and slippage. When backtests ignore these costs, the final results often look much better than what would happen in live trading.

Some strategies accidentally use information that would not have been available at the time the trade was taken. This makes the backtest unrealistic.

Testing a strategy on a small number of trades rarely provides reliable insight. A handful of successful trades does not prove that a strategy has an edge.

Experienced traders often avoid these problems by splitting their data into separate periods. One segment is used to build the strategy, and another is used to test it.

This approach helps reduce the risk of curve fitting.

Both allow traders to practice without risking money, but they serve different purposes.

Backtesting focuses on whether a strategy has potential.

Paper trading focuses on how that strategy feels and behaves in real time.

A strategy might look solid in historical testing but still feel difficult to follow when markets are moving live.

For this reason, many traders progress through a sequence: backtesting first, then simulation or replay trading, and finally real trading with small capital.

FX Replay is designed for this stage, allowing traders to rehearse real market sessions before committing capital.

Traders who take backtesting seriously tend to follow a few basic principles.

Backtesting is rarely a one-time task. Traders often test a strategy, adjust the rules, and test it again to see how the results change.

Conseil de pro

A good backtest should make you skeptical first and confident later.

Backtesting remains the foundation of systematic trading.

Professional traders rely on it because it answers important questions early:

Backtesting doesn’t eliminate uncertainty, but it replaces blind guessing with a clearer understanding of the odds.

Many traders combine backtesting with replay platforms like FX Replay to practice their strategy inside historical market conditions before trading live.

Vous n'avez pas trouvé votre question ici ? Consultez notre centre d'aide ci-dessous !

Centre d'aideBacktesting evaluates a trading strategy using historical market data to see how it would have performed in the past.

No. Backtesting shows how a strategy behaved historically, but future market conditions can always change.

Many traders test strategies across at least five to ten years of historical data so the system experiences multiple market environments.

Adjusting strategy rules until they match past data perfectly but fail when new market conditions appear.

Yes. While it takes more time, manually reviewing charts often helps traders understand how their strategy behaves during different market situations.

.png)