Quarterly Theory Strategy

July 19, 2025

By

Trader Daye

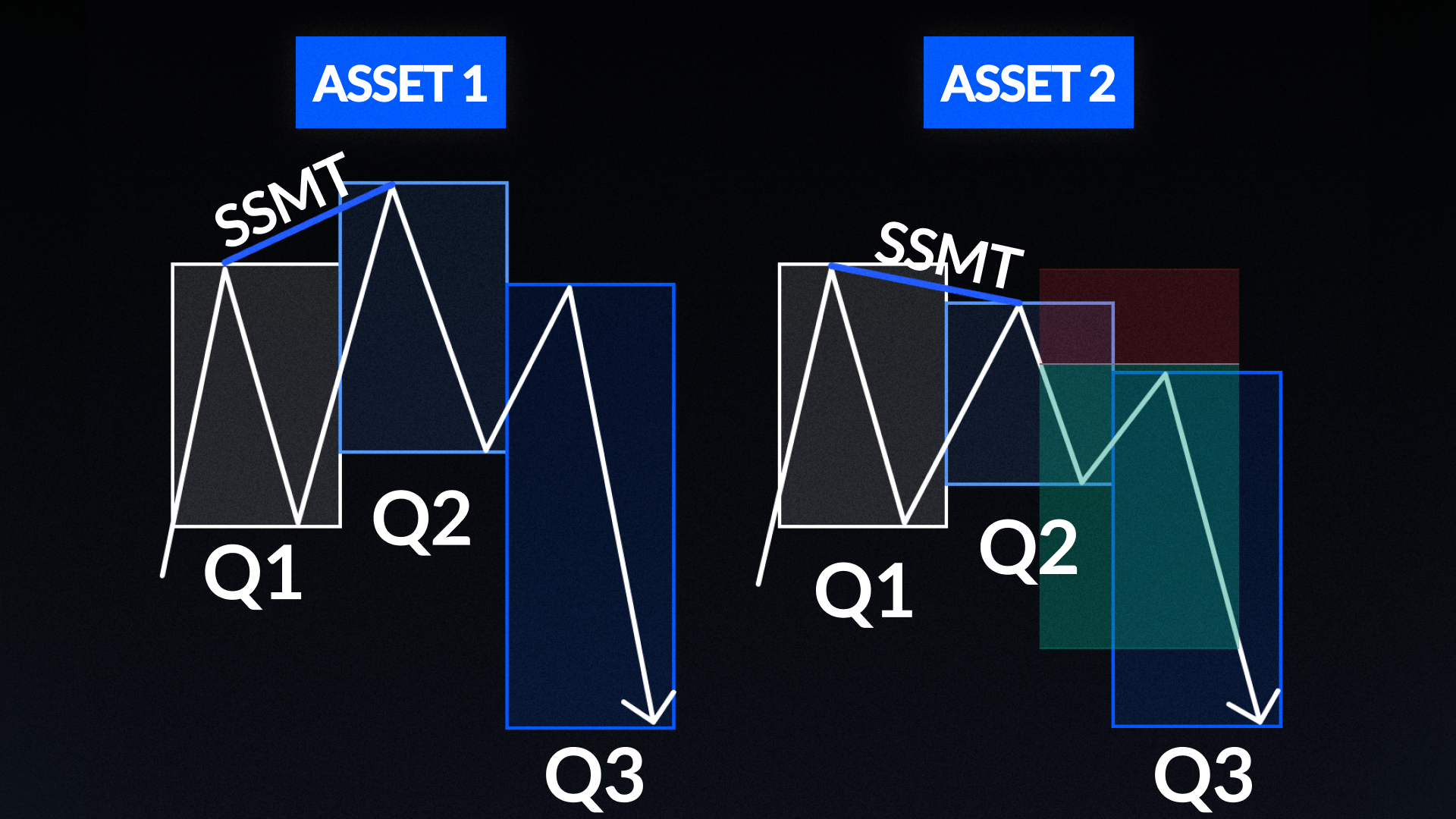

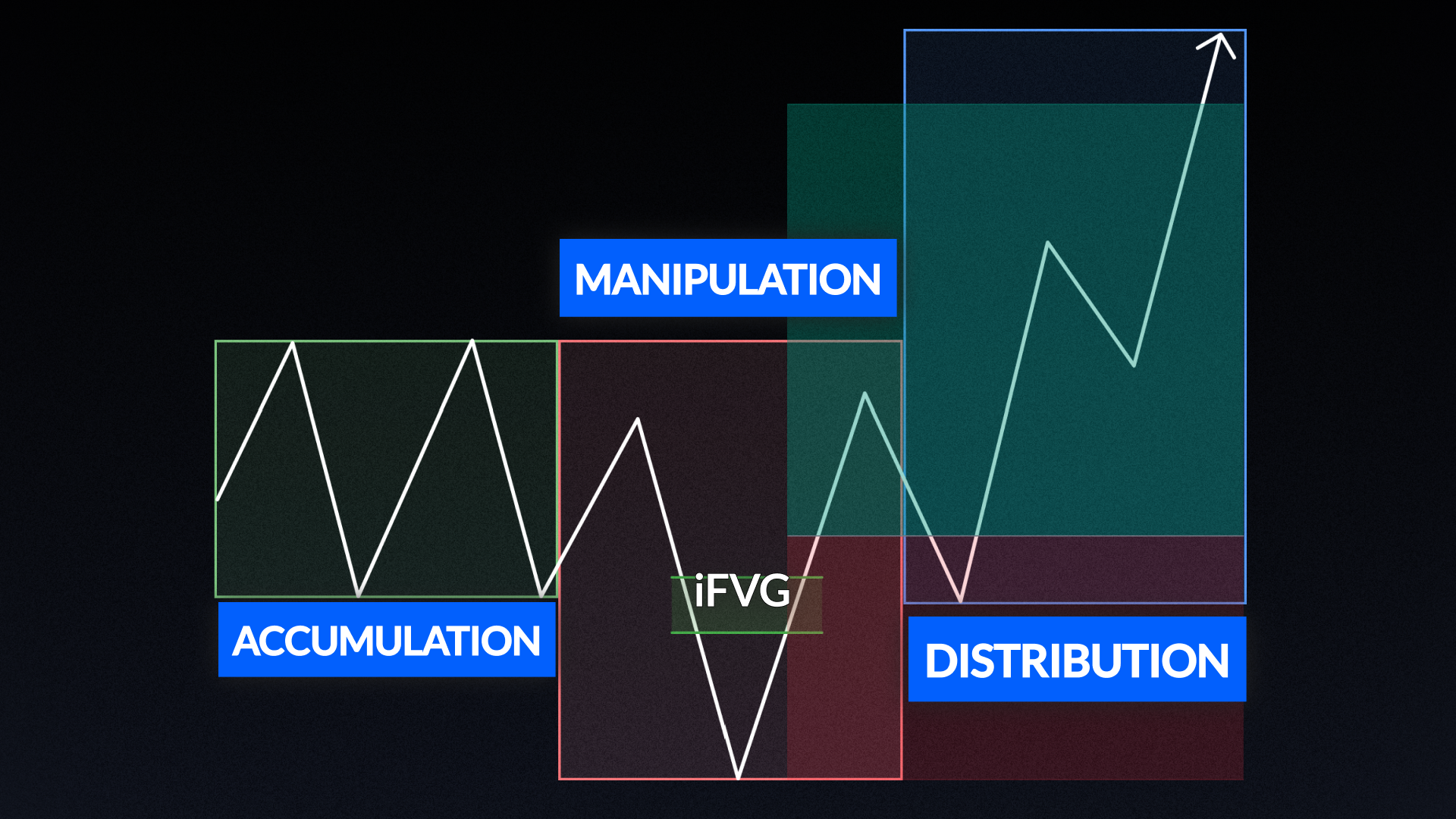

This model uses 90-minute cycles (aka quarters) to map price behavior in structured intervals throughout the session, where each six hour sessions is split into four 90-minute quarters (Q1–Q4). Directional bias can be found through identifying sequential SMT divergence in two or more highly correlated assets between sessions, days, or weeks; where one asset takes out a swing high/low and the other does not.

For lower time-frame entries, look for sequential SMT divergence between 90-minute quarters in correlated assets like EU/GU in London session or ES/NQ in NY session. Trades are only taken 2am - 9am in London session or 9:30am - 15:30pm New York time depending on assets being traded (forex or indices). Entries after either engulfing candle formations or precision swing point candles of different colors between the two assets.

More videos for Quarterly Theory Strategy

Other strategies

By

ICT

By

Waqar Asim