.png)

Most strategies look flawless, until you change the lens.

The entries seem obvious. The exits land clean. The logic holds up when you walk through the examples that made you believe in the idea.

Then you zoom out, change the date range, or switch the market condition, and half of what looked reliable starts falling apart.

That's the difference between a handful of favorable trades and a tested strategy.

Backtesting forces a question most traders avoid until it costs them money: does this actually work across a large enough sample, in different conditions, with costs factored in? Not just in the cherry-picked examples that built the initial conviction.

.png)

Backtesting shows how a defined set of rules performed:

A strategy can show strong backtest results and still fail live because of execution slippage, emotional decision-making, position sizing drift, or simply because the market regime shifted.

Understanding it as a starting point rather than a verdict changes how you approach the whole process.

What a properly run backtest reliably produces:

Without this data, most traders judge a strategy on its last 10 trades. Recency bias drives most early strategy abandonment, and most traders who get stuck in that loop are optimizing based on feeling rather than data.

Dica profissional

Backtesting should challenge your idea. If it confirms everything you expected, you probably didn’t test it properly.

The advantage of proper backtesting is the speed of feedback.

Live trading gives you:

A structured backtesting process compresses that:

The edge comes from repeated exposure to the same decision, across different conditions, until behavior stabilizes.

.png)

This part gets skipped more than any other, and it's the one that determines whether the backtest means anything.

A strategy can't be tested if the rules leave room for interpretation.

"Buy on a pullback to support" isn't a rule. Two traders applying that description to the same chart will find different entries. That ambiguity makes the test meaningless before it starts.

What complete, testable rules look like:

Dica profissional

Write the rules out and have someone else apply them to the same charts. If they find different trades, the rules need tightening.

Data quality is where many backtests quietly break down from bad data inputs.

Common data quality issues to watch for:

Minimum standards for serious backtesting:

If your dataset only contains favorable conditions, the results will be misleadingly favorable.

Each approach serves a different purpose. Most serious traders use a combination of all three.

Manual backtesting

backtesting automatizado

Replay-based testing

The most robust process runs automated testing for statistical validity, manual review for understanding edge cases, and replay to develop execution before going live.

Dica profissional

Manual backtesting improves pattern recognition. Automated testing improves speed. Many traders use both.

Backtesting only produces useful information if the records are complete. Partial logging produces partial conclusions.

Each trade entry should include:

That last item is often skipped and later regretted. Knowing a strategy lost 12 trades is useful. Knowing they came during low-volatility consolidation is actionable, it suggests the strategy only works in trends.

A structured trading journal makes this kind of contextual analysis possible, and it's the difference between traders who improve from a backtest and traders who just run the numbers and move on.

The question worth asking at this stage: what are successful traders actually tracking that the average trader ignores?

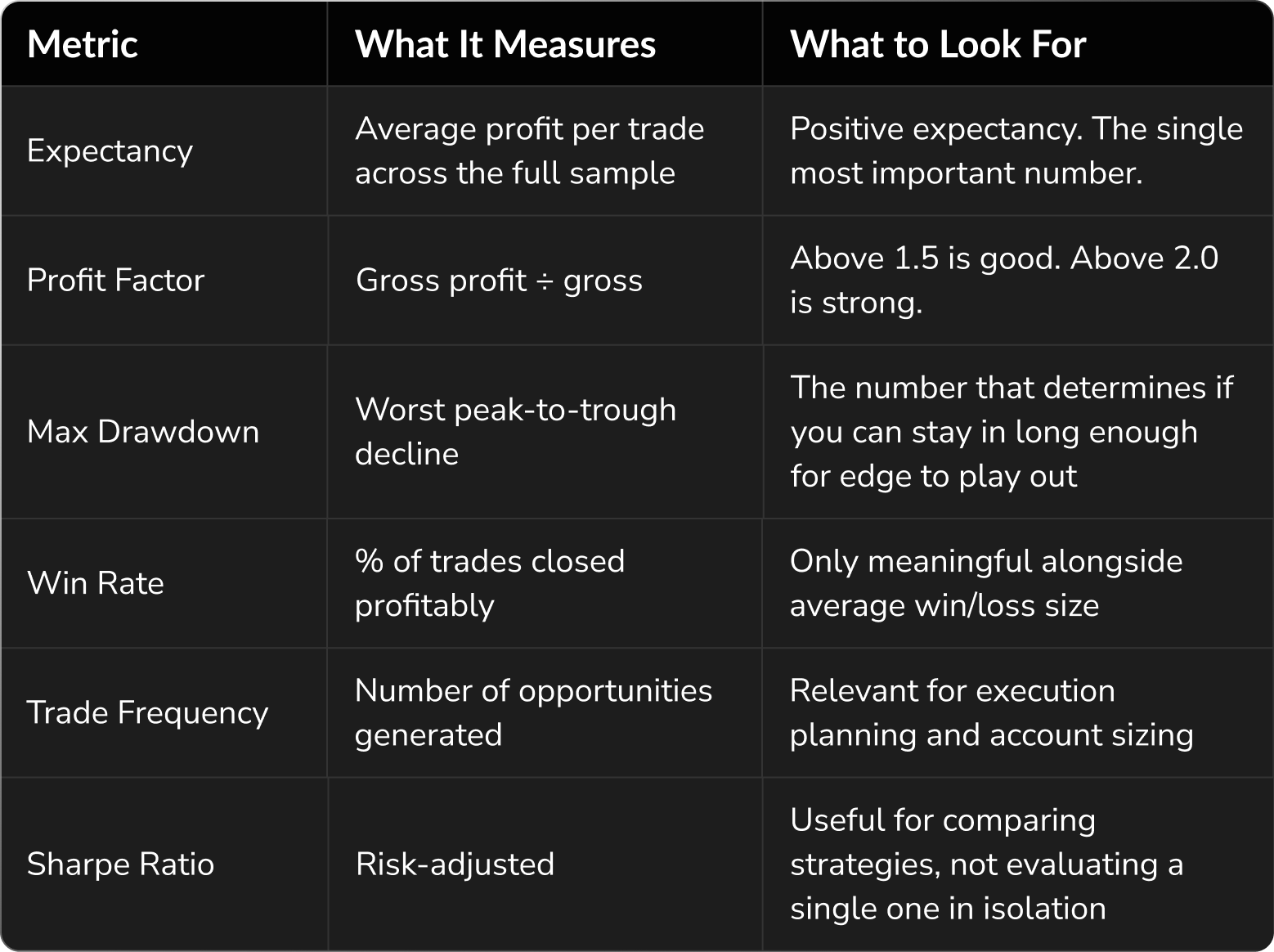

Most traders go straight to win rate. It's intuitive, and it's also the most misleading standalone metric.

A strategy with a 70% win rate can still lose money if the average losing trade is three times the size of the average winner. A 35% win rate can be highly profitable if the reward-to-risk structure is sound.

The metrics that tell a more complete story:

Dica profissional

If the profitable trades are clustered in a short window and the rest of the test is flat or negative, the strategy hasn't demonstrated a consistent edge. It captured a favorable period.

A strategy that only works in trending markets fails roughly half the time.

Markets spend significant periods ranging, consolidating, or grinding through low-volatility phases, and a strategy tested only against a favorable trending period will show results that don't survive real conditions.

Minimum condition coverage for any serious backtest:

This is where replay-based testing becomes especially practical. Instead of relying on your dataset to include the right conditions, FX Replay lets you jump into specific historical periods and trade through them, just as swing traders do to stress-test strategies against less frequent market environments.

.png)

Every backtest reveals something that could be adjusted.

The question is whether the adjustment improves the strategy or just makes the historical numbers look better.

Overfitting (sometimes called curve fitting) is the process of tweaking rules until the historical results look nearly perfect.

The strategy becomes optimized for past data. When conditions shift even slightly, it stops working. This is one of the most common failure modes in strategy development, and it's worth understanding before you spend days adjusting parameters in circles.

Adjustments that make sense:

Adjustments that usually signal overfitting:

Dica profissional

A practical guard against overfitting is out-of-sample testing. Test on one dataset, then apply the same rules to unseen data. If it holds up, the edge is likely real. If not, it’s fitted to history, not the market.

Backtesting validates the statistical case. Forward testing validates execution.

The gap between the two is where most strategies break down.

Slippage, hesitation, and real-time decision-making don’t show up in a backtest. They show up when price is moving and decisions have to be made under pressure.

A sequence that consistently leads to better outcomes:

FX Replay sits in the middle of this process. It bridges the gap between historical results and live trading by allowing practice on real price action, with real timing and decision-making.

For traders preparing for prop firm challenges, this stage is especially critical. Building execution before going live can significantly improve outcomes.

.png)

These issues show up consistently, even among experienced traders.

Rules that work only on the tested dataset. Fix this with out-of-sample validation and restraint when adjusting parameters.

Spreads, commissions, and slippage materially impact results, especially for high-frequency strategies. What looks profitable before costs often isn’t.

20–30 trades aren’t statistically meaningful. Aim for at least 100 trades; 200+ across different market conditions is more reliable.

Using information that wouldn’t have been available at the time. Common in manual testing when future candles influence decisions.

Testing only assets that still exist, which skews results by excluding failures.

A strategy tested only in trending markets will appear stronger than it is. The real test is how it performs across varied conditions.

Traders who use a simulator to catch these mistakes before going live consistently avoid the expensive version of the lesson.

If you want to see the full backtesting and replay workflow before you start, these walkthroughs from the FX Replay YouTube channel cover the process step by step:

Não encontrou sua pergunta aqui?

Consulte nossa Central de Ajuda abaixo!

Most traders consider 100 trades a minimum. 200 or more across multiple market conditions provides meaningfully more confidence.

Yes, particularly for discretionary strategies where execution timing and context matter. It's slower than automated testing, but it builds pattern recognition and situational understanding.

Backtesting applies strategy rules to historical data statistically. Forward testing applies them in real-time or candle-by-candle conditions where execution timing and decision pressure are present.

Once the statistical case is established: a large enough sample, stable metrics across different conditions, realistic costs factored in.

No. Conditions that produced edge historically may not produce it going forward.

A practical guide to backtesting trading strategies step by step. Learn how to define rules, analyze performance, avoid common mistakes, and build a process that holds up before risking capital.

.png)